It is going to take longer than most analysts estimated for Satyam to say ‘all is well’, specifically, at least 18 months

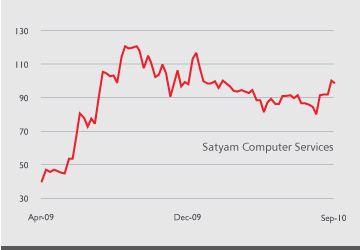

After hitting a 52-week low of Rs78.55 on 31st August, Satyam's share price rose up to Rs114 on 23rd September on hopes of a speedy merger and good results. However, investors were in for a disappointment as restated financials only indicated that the road to recovery for this troubled company is going to be longer than initially expected. Satyam estimates that it will take at least 18 more months to fully convalesce.

A note from Kotak Institutional Equities Research today says, "Satyam faces multiple challenges, including operating with a reduced addressable market, lack of competitive differentiation, loss of quality client base, reduced management bandwidth and high attrition. The new management has done a creditable job in holding the organisation together, but we believe a meaningful turnaround is some time away."

What Satyam disclosed yesterday is this: revenues of Rs54.8 billion in FY10, EBITDA margin of 8%, net loss of Rs1.2 billion after including extraordinary items of Rs4.2 billion [relating to severance compensation for employees (almost Rs1 billion), forensic investigation expenses (Rs1.1 billion), and write-down in value of assets of subsidiaries (Rs2.2 billion)], cash and cash equivalent of Rs22 billion as of 31 March 2010 (but Rs19 billion after payout for the Upaid dispute) and accumulated losses of Rs27.5 billion.

The balance sheet impact of the fraud committed by Raju has been about Rs69 billion. Satyam had just 27,000 employees at the end of FY10 and plans about 3,000 campus hires this year. However, it is still unclear about hiring at a senior level for 2010.

In a televised interview, Vineet Nayyar, chairman; CP Gurnani, CEO and S Durgashankar, CFO of Mahindra Satyam disclosed that its main revenue contributors are US (2/3rd) and Europe (15%-20%).

The market is disappointed that it did not disclose whether there will be a tax shield available on accumulated losses, some details of FY10 such as Q4 revenue run rate and margin and details on any operational metrics.

Brokerage reports after Satyam's disclosures are far from euphoric. CLSA's note to its institutional clients today says, "Through the last 15 months, we have been advising investors to stay away from the Satyam-Tech Mahindra combine.

Satyam's reported financials for FY10 do nothing to change our view." It talks about five key truths which will drive investment decisions in Tech Mahindra-Satyam in the future - Satyam's FY10 revenues are not representative of its future revenues.

CLSA expects 2HFY10 revenues to be lower than 1H as clients who initially did not pull out subsequently cancelled contracts. FY11 revenues are likely to be lower than FY10 because it could not participate in a lot of deals because its financials were not ready and the company had high attrition creating supply side pressures. CLSA believes Satyam will trail industry revenues in FY12 as well as IT services is a 'game of scale' and Satyam is lagging behind too much.

A merger with Tech Mahindra may not change things much feels CLSA - "While a merger with Tech Mahindra does give Satyam some scale, it does not give it the muscle to compete with larger peers in sectors outside telecom." Satyam's margins will improve going forward but not rapidly as it will have to make pricing compromises to win deals. "Risk-reward is favourable neither in Satyam nor in Tech Mahindra," concludes CLSA.

CLSA's bull case estimates for Satyam are revenue at $1.2 billion or Rs54.6 billion in FY11 and $1.4 billion or Rs62.8 billion in FY12 and EBITDA of Rs7 billion and Rs10.4 billion - CLSA assumes margins doubling in two years. Assuming a tax rate of just 5% it will earn a profit of Rs6.2 billion and Rs9.7 billion. Kotak estimates FY11 and FY12 revenues at $1.1 billion and $1.3 billion and profit at Rs5.9 billion and Rs6.3 billion, based on the assumption that FY11 revenue growth will be -5%, FY12 at 22%, FY11 employees at 31,050 and FY12 at 36,329, employee additions at 4,050 and 5,279 and utilisation rate at 77% after being at 68%.

The Kotak report points out a couple of challenges that Satyam faces - it says that Satyam's $800 million revenue loss from 150 clients implies that it lost $5 million of revenue per customer. This is high compared with its current revenue per client at $3.3 million. The second big challenge is the loss of almost its entire management team. Kotak says, "We understand that only four members of the 42 key members of the senior team of Satyam are still with the company."

(This article is based on secondary research. The report is for information only. None of the stock information, data and company information presented herein constitutes a recommendation or solicitation of any offer to buy or sell any securities. Investors must do their own research and due diligence before acting on any security. Some of the opinions expressed in this article are the author's own and may not necessarily represent those of Moneylife).— Munira Dongre

.jpg "MoneyLife")