Oil, metals, banks and auto expected to lead December quarter growth

January 7, 2011

Oil & gas, metals, banks and auto sectors will drive earnings; cement and telecom are expected to lag behind; low base effect may be over for the Sensex from this quarter, according to a brokerage house

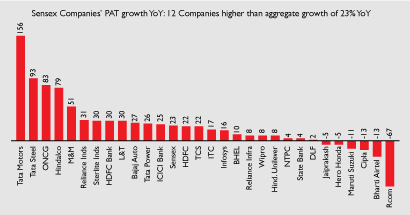

An important factor to keep in mind when looking at the October-December 2010 quarter results, says Motilal Oswal (MOSL), is that the low base effect is almost over. At an aggregate level, the Sensex PAT growth was 23% in 3QFY10 and the brokerage expects it to be 23% for 3QFY11. Oil & gas, metals, banks (especially private banks) and auto sectors are expected to perform well, while cement and telecom will probably be laggards. The pharmaceutical sector is also expected to do well.

MOSL states in its December quarter earnings preview report, "Nine of the top 10 earnings growth companies in the Sensex are expected to be from autos (Tata Motors, M&M), commodities (Tata Steel, ONGC, Hindalco, Reliance Industries, Sterlite), and private banks (HDFC Bank, ICICI Bank). Telecom is the biggest drag on Sensex PAT growth with Reliance Communications' PAT expected to be down 67% year-on-year and Bharti's PAT (may be) down 23%."

With reference to the auto sector, MOSL expects volumes to be strong. An increase in end prices may cushion margins somewhat, but overall EBITDA levels are expected to come off a bit due to higher raw material prices.

Going forward, the auto sector is expected to face headwinds in the form of higher interest rates, steeper fuel prices, and higher product prices. This could be a trend across consumer-driven sectors in India, which is why MOSL says that export-driven sectors could perform better than domestic ones.

The report says, "We believe near-term challenges will impact performance of several sectors, particularly those dependent on domestic markets. We expect rising input costs, fuel prices and interest rates to impact discretionary consumption spends including (the) auto (sector). In this backdrop, global commodities and export-oriented sectors like technology and pharma would continue to outperform."

For the December quarter, in banking, MOSL expects credit growth to remain strong, but deposit growth to lag, putting pressure on net interest margins. Further clarity is expected on pension and gratuity related liabilities. Margins seem to have peaked for this sector, the brokerage believes.

Cement demand momentum is muted with volume growth of 7.3% year-on-year, but down almost 10% quarter-on-quarter. Domestic prices are about 7% higher quarter-on-quarter and 4.5% year-on-year.

Overall EBITDA margins may improve quite a bit quarter-on-quarter, but they are still down almost 800 basis points year-on-year. MOSL believes prices have bottomed out and that utilisation will improve from here.

The construction sector is expected to benefit from order flows from the National Highways Authority of India (NHAI) and the building segment after a sluggish first half. Construction costs and interest rates will rise, but MOSL expects "EBITDA and net profit margins to stabilise with growing composition of higher margin contracts in the order book."

Growth in the FMCG sector is expected to be volume-led, as very few have taken price increases. Although input costs have risen, players haven't passed all of them on. But this may not impact margins yet because of cost cuts.

The information technology (IT) sector is expected to see 5%-7% topline growth; commentary on near-term prospects is expected to be bullish; and rupee appreciation will hurt margins.

In metals, domestic steel demand and pricing was sluggish and only picked up towards December. "The shutdown of Ispat Industries in November helped in a supply-side correction. Improved price sentiment globally helped in recovery of prices in the domestic market." Margins may be under pressure due to higher iron ore prices. Zinc and aluminium prices have been strong and may reflect in earnings.

Inventory gain is seen for oil & gas companies, as crude gained $10 per barrel this quarter. It also expects strong GRMs (gross refining margins), led by naphtha cracks. Polyester margins were strong but polymer margins were weak. Despite a number of new launches, real-estate sales momentum could have been impacted due to sharp rise in prices and higher interest rates, says the brokerage.

In telecom, MOSL expects a revival of revenue and operating profit growth after a sluggish September quarter, "driven by a seasonal volume uptick and relatively stable pricing environment." For utilities, imported coal prices were higher and merchant prices continued to be lower.

(This article is based on secondary research. The report is for information only. None of the stock information, data and company information presented herein constitutes a recommendation or solicitation of any offer to buy or sell any securities. Investors must do their own research and due diligence before acting on any security. Some of the opinions expressed in this article are the author's own and may not necessarily represent those of Moneylife.) — Munira Dongre

.jpg "MoneyLife")